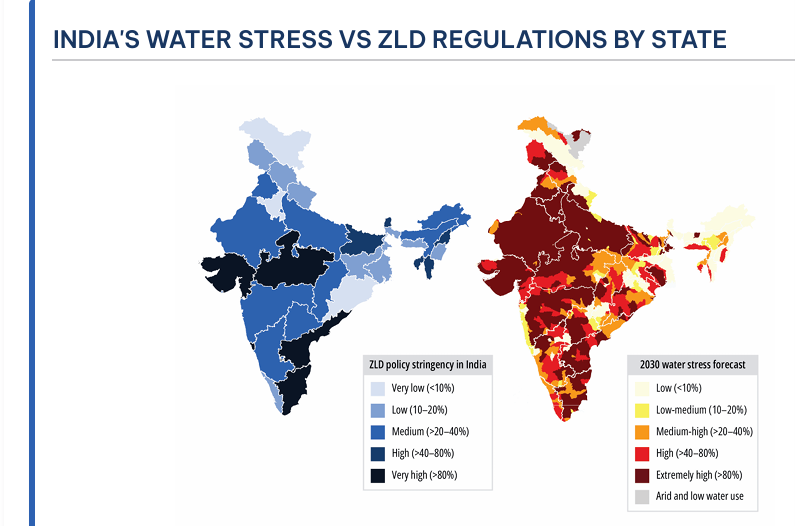

India is rapidly becoming one of the most important markets for zero liquid discharge (ZLD). Water stress, industrial expansion, and tightening regulations are all converging.

A recent GWI interview with Siva Kumar Kota, Head of Technology, makes it clear: the fundamentals are in place, but adoption has lagged.

At Gradiant, we see three factors determining what happens next: enforcement, economics, and ecosystem.

ZLD in India has largely been a compliance-driven decision. High energy costs, inconsistent enforcement, and limited value recovery have slowed adoption. Conventional thermal systems remain widespread, but they are increasingly challenged on cost and efficiency.

That is changing.

New industries, including semiconductors, solar PV manufacturing, and battery recycling, are deploying ZLD from day one. These sectors demand advanced treatment, faster deployment, and higher recovery.

This is where the market shifts.

ZLD is moving from cost center to value driver.

Advanced technologies such as CFRO and CGE are reducing energy intensity, improving recovery, and enabling modular deployment. Just as important, integrated systems are unlocking reuse and resource recovery pathways.

India’s ZLD market is at an inflection point. The question is no longer whether ZLD will scale. It is how quickly.

The opportunity is not just to meet compliance. It is to turn wastewater into a strategic advantage.